July 25, 2025

3 mins

Prerana Jakkidi

July 25, 2025

3 mins

Why Today’s Rate Environment Demands a Smarter Cash Strategy

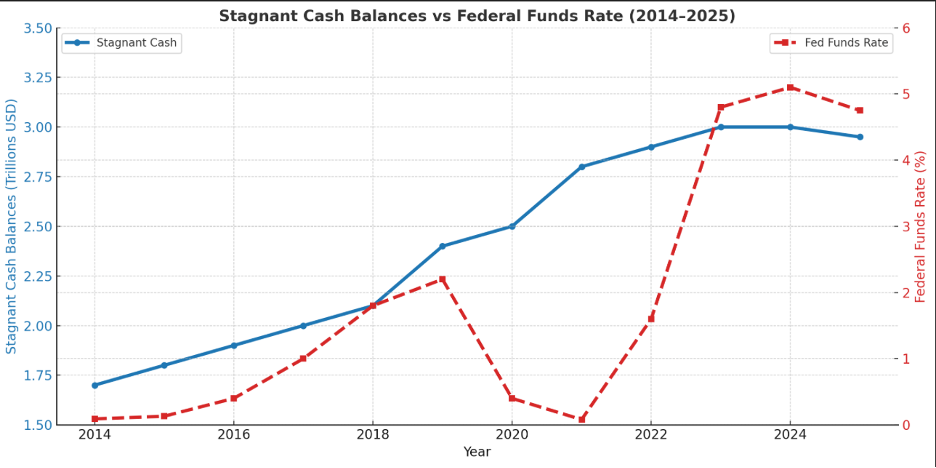

Over the last two years, the U.S. has witnessed one of the fastest interest rate hikes in modern monetary history. Yet despite rates reaching multi-decade highs, over $3 trillion in U.S. bank deposits remain parked in accounts earning 0%, according to FDIC data. A significant portion of this from corporations, advisory firms, and professional services businesses is effectively stagnant capital, losing real value in inflation-adjusted terms.

JPMorgan alone holds over $600 billion in non-interest-bearing balances—over 30% of its total deposits (Financial Times, 2024).

For CFOs, controllers, and financial advisors, this is more than a missed opportunity, it’s a strategic oversight. In an inflationary economy, holding excess cash without yield is a silent cost. A modern approach to cash management isn’t just about liquidity it’s about segmentation, optimization, and institutional-grade capital efficiency.

A Bucketed Cash Strategy – Reframed for Financial Decision Makers

A tiered cash model helps organizations assign purpose, align timeline, and unlock value across their cash positions. Below is a professionalized version tailored for financial executives:

1. Operating Liquidity (0–30 Days)

These are immediate cash needs — payroll, AP, short-term vendor payments, client reimbursements.

2. Strategic Reserves (30–180 Days)

Funds earmarked for contingencies, tax payments, or seasonal business needs.

3. Planned Capital Allocation (6–18 Months)

Funds set aside for equipment purchases, expansion, M&A due diligence, or debt service.

Institutional Implications: Why It Matters for Advisory and Accounting Firms

Advisory and professional services firms often hold significant retained earnings or client pass-through funds. Optimizing this capital offers three major benefits:

In an era of elevated interest rates and persistent inflation, letting cash sit idle is no longer defensible. By segmenting capital into purpose-driven buckets and leveraging modern tools like sweep networks, custodial platforms, and short-duration instruments, CFOs and advisors can transform stagnant cash into a strategic asset. The opportunity cost of inaction is real—and in today’s environment, intentional cash management isn’t just smart finance; it's a competitive advantage.